What is Philippine Airlines actually buying from oneworld?

- Krishnan Srinivas

- Jun 15

- 13 min read

In Brief: Philippine Airlines has 4 percent of its home market and just signed to join a global alliance. Over two decades, low-cost carriers across Southeast Asia absorbed the domestic volume while flag carriers retreated to the segment LCCs do not contest. Corporate travel, loyalty ecosystems, and premium long-haul yield denominated in dollars. PAL is the sixth Southeast Asian flag carrier to follow the same sequence across Indonesia, Malaysia, Thailand and Vietnam. The move was visible six years before the announcement. This piece examines the bilateral trail that made it inevitable, what the pattern looks like across the region, and whether PAL's balance sheet and Manila's geography make the return on this investment real

Download full analysis as a PDF or continue reading below:

Philippine Airlines (PAL) signed a memorandum of understanding to join oneworld on 6 June 2026, becoming the alliance's 16th member and only the second full member based in Southeast Asia. The first being Malaysia Airlines.

The announcement may look like a network expansion story. It is better understood as the formalisation of a strategy PAL has been pursuing for several years. The airline has steadily built commercial ties with oneworld members through codeshare agreements, loyalty partnerships and fleet investments designed to support long-haul growth.

PAL's move reflects a pattern already visible across Southeast Asia. Across Southeast Asia, low-cost carriers captured domestic volume while flag carriers increasingly relied on international networks, premium traffic and loyalty ecosystems to sustain profitability. PAL's move offers a useful case study in how a flag carrier responds once domestic scale is no longer its primary advantage.

Why it was coming and what it means for oneworld

The timeline shows that the June 2026 announcement did not emerge suddenly. PAL spent several years building bilateral relationships with key oneworld members before formalising the alliance relationship. American Airlines provided an early codeshare link. Alaska Airlines, Qatar Airways and Qantas followed with loyalty and commercial partnerships. The MoU effectively consolidates relationships that already existed into a single alliance framework.

This matters because alliances rarely create traffic from scratch. More often, they institutionalise traffic flows, loyalty relationships and commercial cooperation that have already proven valuable. In PAL's case, the announcement reflects a strategy reaching its logical conclusion rather than a new strategic direction.

For PAL, alliance membership strengthens the economics of a network that increasingly depends on international passengers rather than domestic scale. PAL Express provides domestic feed from across the Philippine archipelago into Manila, where passengers connect onto PAL's long-haul network. Oneworld expands the pool of passengers who can access those flights while making the airline more attractive to corporate travellers and frequent flyers who value alliance benefits.

The logic works in both directions. PAL gains access to a larger loyalty ecosystem, broader distribution channels and additional feed from alliance partners. Oneworld gains a Manila hub and access to destinations across the Philippines that remain underserved by existing members. The addition complements rather than overlaps with Cathay Pacific and Japan Airlines, particularly for traffic flows involving Australia, North America and secondary Philippine cities.

The question, however, is why this logic has become increasingly important for PAL. The answer begins with the structure of the Philippine domestic market.

What Philippine’s domestic market reveals

The Philippines domestic market is one of Southeast Asia’s most LCC-dominated aviation markets. Over the past two decades, low cost carriers have captured majority of the domestic traffic through lower fares, dense point-to-point networks and aggressive capacity deployment. While Philippine Airlines remains the country’s flag carrier, it now operates within a market where scale increasingly sits outside the full-service segment.

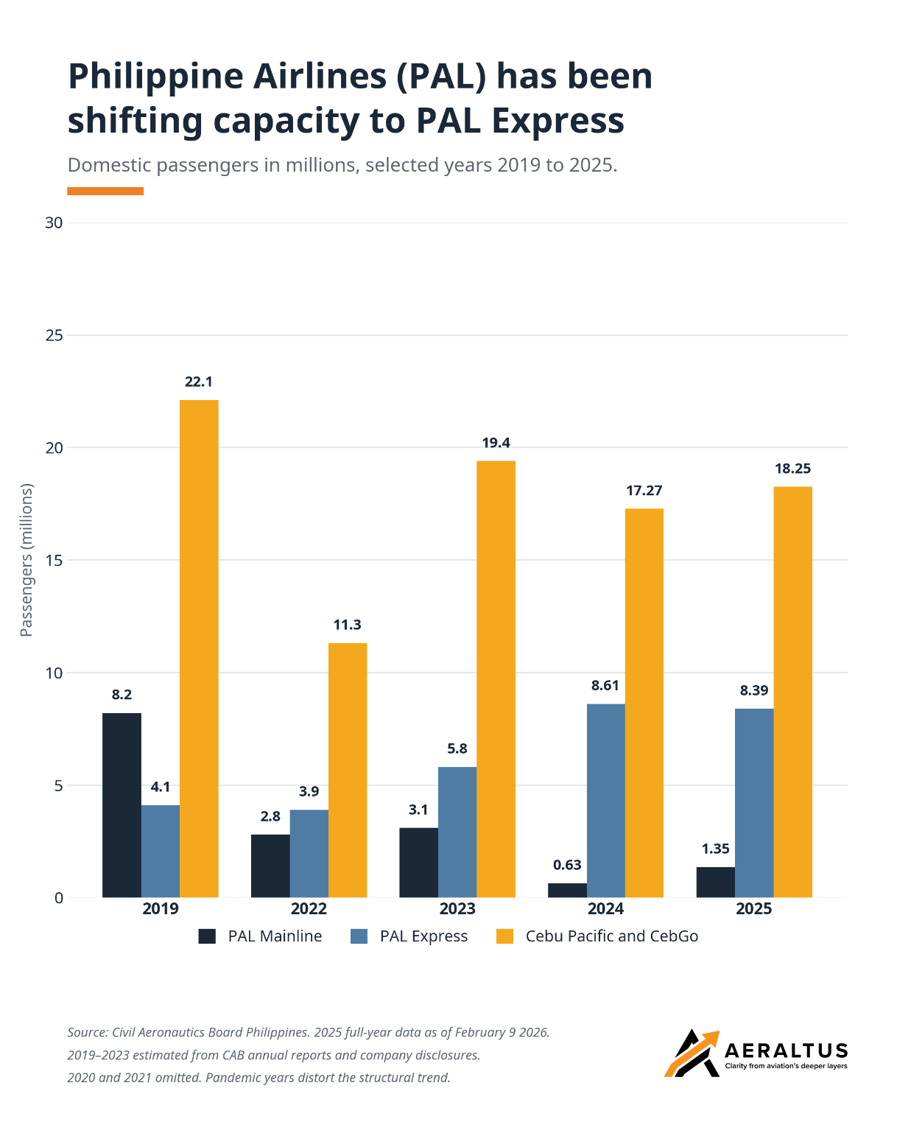

The significance of this market structure is that PAL no longer controls domestic volume. PAL mainline accounts for just 4% of domestic passengers, while most of the group’s domestic traffic sits within PAL Express. This reflects the broader strategic reality that PAL cannot compete with Cebu Pacific on domestic scale and has instead separated domestic volume from the mainline operation. This has resulted in a group structure where PAL Express carries much of the domestic network, while Philippine Airlines concentrates on international and higher yield markets. The next figure shows how this shift has accelerated over time, with domestic passenger volumes moving steadily from the mainline carrier to PAL Express.

This shows that PAL increasingly treats its domestic network as a feeder and connectivity platform than a core profit engine for the mainline carrier. The traffic now being concentrated to PAL Express, allows the mainline to focus on aircraft and resources on higher-yield international markets such as Australia, North America and North Asia. The shift in capacity to PAL Express has been gradual right from the pandemic, the restructuring and now as per the latest numbers with PAL Express effectively handling 86% of the group’s domestic passenger traffic, while PAL mainline accounts for 14%.

The pattern across Southeast Asia

PAL’s domestic position is not unique. Across Southeast Asia, full-service flag carriers faced the same competitive dynamic once low-cost carriers expanded aggressively during the 2000s. As fares fell and air travel became accessible to a much larger segment of the population, traffic growth increasingly accrued to LCCs rather than the incumbent flag carrier. The result was a structural shift in market share that reshaped the role of the region’s legacy airlines.

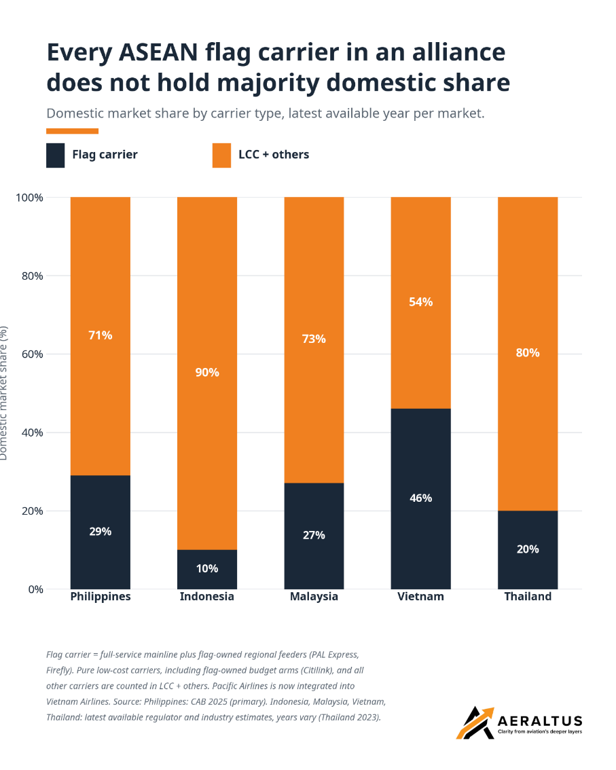

The common feature across alliance-affiliated ASEAN flag carriers is that none retains a majority share of its domestic market. In the Philippines, Indonesia, Malaysia and Thailand, domestic volume now sits primarily with LCCs and their affiliates. Even Vietnam Airlines, the strongest performer in the group controls less than half of domestic passengers. The domestic market therefore ceases to be the primary source of competitive advantage. Instead, the flag carrier’s role shifts toward protecting international connectivity, premium traffic, corporate accounts, and long-haul markets that remain less vulnerable to low-cost competition.

The response has been remarkably consistent. Most flag carriers either launched or expanded lower-cost subsidiaries to absorb domestic volume while preserving the mainline carrier for higher-yield international operations. Garuda Indonesia developed Citilink, Malaysia Airlines expanded Firefly, Vietnam Airlines operated Pacific Airlines and VASCO, while Philippine Airlines relied on PAL Express. Singapore Airlines despite having no domestic market but also facing stiff competition in the regional connections, launched Scoot. Although the structures differ, the underlying logic is similar, which is to separate volume from yield.

Indonesia provides one of the clearest examples. LCC and regional subsidiaries account for roughly 90% of domestic passengers and Garuda’s low cost subsidiary Citilink carries more passengers than the mainline carrier. Following its restructuring, Garuda reduces its mainline footprint and concentrated on international and premium markets while maintaining SkyTeam membership.

Malaysia Airlines and Thai Airways sit at different points on the same trajectory. Both operate in markets where LCCs dominate domestic traffic, leaving the flag carrier to compete primarily through network connectivity, premium service and international reach rather than domestic scale. Following its restructuring, Thai Airways absorbed Thai Smile into the mainline operation, effectively bringing domestic feed directly into the Star Alliance network.

Therefore, the broader implication is that once a flag carrier loses domestic scale, alliance membership becomes more important, because the carrier’s value increasingly comes from network connectivity and international revenue rather than domestic market leadership.

PAL’s financials and what this means for the return they are seeking

If the ASEAN pattern explains why alliance membership becomes attractive, it does not explain why PAL chose to pursue oneworld membership now. Alliance participation requires investment in systems integration, loyalty program alignment, interline capability and service standards. A carrier under financial stress can postpone those costs. However, the relevant question is therefore whether PAL’s post-bankruptcy recovery has reached the point where management can justify making that investment.

PAL’s financial trajectory suggests the decision follows recovery rather than precedes it. Following its Chapter 11 restructuring, the airline moved from a USD 255 Million loss in FY21 to sustained profitability, while passenger increased by 57% in FY2025. The significance is that management now has the balance-sheet flexibility to invest in capabilities whose return Is measured over years rather than quarters. Alliance membership is one such investment.

The question therefore shifts from whether PAL can afford alliance membership to what return management expects from it. If the domestic volume war has already been lost, alliance membership must generate value elsewhere. The investment case rests on whether oneworld can help PAL defend premium revenue, retain high-value customers and strengthen the international network that increasingly underpins the airline’s economics.

Alliance membership does two things that matter here, and both relate directly to the return PAL is seeking on the investment.

The first return is defensive: protecting revenue that already exists. Once a flag carrier loses domestic scale, it cannot rely on market share alone to retain its highest-value customers. Corporate travellers, frequent flyers and premium leisure passengers increasingly compare networks rather than airlines. The question becomes less whether PAL flies a particular route and more whether a PAL customer can earn, redeem and receive recognition across a global footprint.

For PAL, this matters because the most valuable part of the business increasingly sits outside the domestic market. Routes to North America, Australia and the Middle East generate dollar-denominated revenue, while a large share of aircraft lease and maintenance obligations are also denominated in dollars. Every premium passenger retained within the Mabuhay Miles ecosystem is therefore more valuable than an additional domestic passenger travelling on a price-sensitive route. Alliance membership helps protect that revenue base by making PAL a viable alternative to larger loyalty ecosystems such as KrisFlyer, Mileage Plan or Qatar Airways Privilege Club.

The second return is offensive: generating traffic that PAL would struggle to capture independently. Alliances widen distribution, create additional feed and place an airline's flights inside partner sales channels. The value of this function depends entirely on geography. A carrier located away from major connecting flows receives the defensive benefits but captures limited network upside.

Garuda Indonesia illustrates the distinction. SkyTeam membership provides access to a global loyalty and partnership framework, helping retain premium customers despite intense domestic LCC competition. What it does not provide is a meaningful sixth-freedom opportunity. Jakarta sits away from the primary North Asia-ASEAN and transpacific flows. The alliance therefore protects revenue without materially changing Garuda's role within the regional network.

PAL enters oneworld from a different position. Manila sits at the intersection of North America, North Asia, Australia and Southeast Asia. That geography creates the possibility of capturing additional connecting traffic through the Philippines rather than simply defending existing passengers. PAL could add destinations in the US that are hubs of their alliance partners American Airlines such as Dallas, Miami, Philadelphia and/or Charlotte using the A350-1000s that could help it leverage domestic connections. Every additional passenger placed onto a PAL-operated long-haul flight by American Airlines, Alaska Airlines, Qantas or Qatar Airways represents revenue PAL would otherwise have had to acquire itself.

Therefore, if the alliance functions primarily as a defensive tool, the return should appear through stronger yields, loyalty retention and premium-cabin performance. If the offensive opportunity materialises as well, PAL should also see growth in sixth-freedom traffic and partner-generated feed through Manila. The observable question is which of these outcomes appears first, and at what scale.

What would prove this wrong

The argument rests on a simple proposition: PAL has accepted the loss of domestic scale and is using oneworld to strengthen the international business that remains. If that is true, the evidence should appear in the airline's network, traffic mix and revenue profile over the next several years. Four questions are worth tracking.

1. Will PAL continue treating the domestic market as a feeder network? The thesis assumes PAL has stopped competing for domestic volume and instead uses the domestic network to support international flying. The evidence so far points in that direction. PAL Express now carries more than six times the domestic passenger volume of PAL mainline, while the mainline operation concentrates on international markets.

A different outcome would challenge the argument. If PAL begins rebuilding a large domestic mainline presence, adding capacity on routes such as Manila-Cebu and Manila-Davao to compete directly with Cebu Pacific on frequency and volume, management would be signalling a return to the domestic market share battle. Civil Aeronautics Board filings and annual passenger data will show whether PAL continues separating domestic volume from the mainline business.

2. Can ASEAN flag carriers achieve the same outcome without an alliance?

A second assumption runs throughout this analysis: once a flag carrier loses domestic scale, alliance membership becomes the most effective way to protect premium revenue and network relevance. That assumption remains largely untested. No major ASEAN flag carrier facing sustained LCC pressure has built an equivalent global proposition through bilateral partnerships alone. If another carrier succeeds in doing so, the strategic value of alliance membership becomes less certain. The question is whether alliances are necessary or simply the most established solution currently available.

3. Will Manila become a genuine connecting hub? This analysis frames oneworld primarily as a yield-defence strategy. Manila's geography creates the possibility of something larger. If PAL begins attracting meaningful traffic flows between North America, North Asia, Australia and Southeast Asia, alliance membership becomes more than a defensive tool. In that scenario, oneworld is helping PAL build a sixth-freedom proposition rather than simply protecting existing revenue streams. Passenger flows through Manila will reveal whether PAL remains predominantly an origin-and-destination carrier or evolves into a connecting hub.

4. Can premium demand support PAL's long-haul strategy? Ultimately, the economics must work in the premium cabin. PAL's incoming A350-1000 fleet carries 42 business-class suites on transpacific routes. The investment case strengthens if those seats consistently attract corporate travellers and premium leisure passengers who value alliance benefits, loyalty recognition and network connectivity. It weakens if demand remains concentrated in price-sensitive OFW and diaspora traffic that primarily books economy seats. PAL itself has acknowledged the price sensitivity of parts of the Filipino diaspora market. The key indicators therefore sit in the premium cabin such as business-class load factors, premium yields and revenue performance on long-haul routes. Those metrics will reveal whether the customers oneworld is designed to retain are actually choosing PAL.

The answers to these questions will determine whether oneworld functions primarily as a defensive shield, a platform for network expansion, or an investment whose returns fall short of expectations.

Closing Thoughts

PAL's oneworld entry is significant because it reveals how the economics of Southeast Asian aviation have changed. For most of the jet age, domestic scale formed the foundation of a flag carrier's business. The domestic network generated passengers, market power and loyalty that could support international growth. Across much of Southeast Asia, that relationship has reversed. Low-cost carriers now control most domestic passengers, while flag carriers increasingly rely on international routes, premium traffic and global partnerships to sustain profitability.

PAL is joining oneworld after domestic volume has shifted elsewhere and after restructuring created the financial flexibility to invest in long-term revenue protection. Alliance membership is no longer about extending network reach from a position of domestic strength. It is about protecting the international business that remains once domestic scale is gone. PAL's answer is oneworld. Whether that proves to be a defensive shield or a platform for a larger connecting hub through Manila will become clear over the next several years.

Author's Note

This analysis is based on public information such as listed filings, reports. The open questions are genuine and not rhetorical. Aeraltus does not hold a position in Philippine Airlines, oneworld or any related entity.

About Aeraltus

Aeraltus produces structural aviation analysis and intelligence on emerging markets across Indian subcontinent, ASEAN and Africa. Custom aviation analysis is available for aviation industry professionals that include institutional investors, airline strategy teams, lessors and corporate development groups. If you want a tailored read on a specific carrier, route system, fleet decision or deal, using data that can’t be discussed publicly, Aeraltus runs bespoke engagements alongside the published work. Contact info@aeraltus.com.

Sources

1. Philippine Airlines press release: "Philippine Airlines to Join oneworld Alliance." 6 June 2026. PAL.com.

2. FlightGlobal: "Philippine Airlines to join Oneworld." 6 June 2026.

3. Aerotime: "Philippine Airlines joins oneworld, becoming the alliance's 16th member." 7 June 2026.

4. Context.ph: "Cebu Pacific stays on top as PH lead domestic airline." 24 February 2026. Citing Civil Aeronautics Board 2025 full-year data.

5. Malaya Business Insight: "Cebu Pacific solidifies position as largest PH airline in domestic market." February 2026. Citing CAB 2025.

6. Rappler: "Cebu Pacific, Philippine Airlines cancel, limit select flights due to oil price hike." April 2026. Citing Cebu Pacific 2025 full-year results.

7. Qatar Airways Newsroom: "Qatar Airways and Philippine Airlines Strengthen Partnership, Expand Markets and Benefits for Loyalty Members." 18 May 2026.

8. Business Traveller: "Qantas Expands Philippine Airlines Partnership: New Destinations to Redeem." June 2026.

9. CGAA.org: "Philippine Airlines Airline Alliance Expands Global Reach." September 2025. On Alaska Airlines partnership.

10. PAL Holdings, Inc.: Annual Reports FY2023, FY2024, FY2025. phi.com.ph/financial-reports. Primary peso net income figures: P16.81B (FY2023), P7.02B (FY2024), P9.62B (FY2025). Peso-to-USD conversion at 56 PHP/USD applied consistently across FY2023–FY2025 for Figure 4.

11. Manila Times: "PAL welcomes arrival of second Airbus A350-1000 aircraft." 31 May 2026.

12. Aircraft Interiors International: "Philippine Airlines (PAL) reveals its A350-1000 cabin interiors." February 2026.

13. Jakarta Globe: "Lion Group Controls 60% of Domestic Aviation Market." November 2022. Citing INACA annual report. Used for Indonesia LCC structural claim alongside INACA 2024 estimate; note that post-restructuring Garuda mainline share figure (approximately 10%) is drawn from INACA 2024 via academic secondary sources, not primary INACA filing. The 10% figure should be treated as an estimate.

14. The Edge Malaysia: "Garuda Indonesia loss widens as scheduled airline revenue slips." 18 March 2026. Citing Garuda Indonesia financial statements filed to the Indonesia Stock Exchange (FY2025 net loss: US$323 million).

15. SkyTeam press release: "Garuda Indonesia joins SkyTeam." 5 March 2014. skyteam.com. (SkyTeam membership date.)

16. MAVCOM (Malaysia Aviation Commission): Annual reports. Malaysia market share figure is an estimate for 2024; primary MAVCOM filing not independently verified for this piece. Treat as directionally accurate, not precisely sourced.

17. CAAT (Civil Aviation Authority of Thailand): Traffic statistics. Thailand market share figure is an estimate for 2023, the most recent year available via secondary sources at time of writing.

18. CAAV (Civil Aviation Authority of Vietnam): Traffic statistics. Vietnam market share figure is an estimate for 2025 from secondary sources; primary CAAV filing not independently verified.

19. INACA (Indonesia National Air Carriers Association): Annual report 2024, cited via Jakarta Globe and academic secondary sources. Indonesia market share figures are estimates; the primary INACA filing was not directly accessed.

20. oneworld press release via PAL.com: member airline listing as of June 2026.